It Comes Down to Your DTI

-

by Jamohl DeWald

by Jamohl DeWald

- December 16, 2024

- Uncategorized

- 0

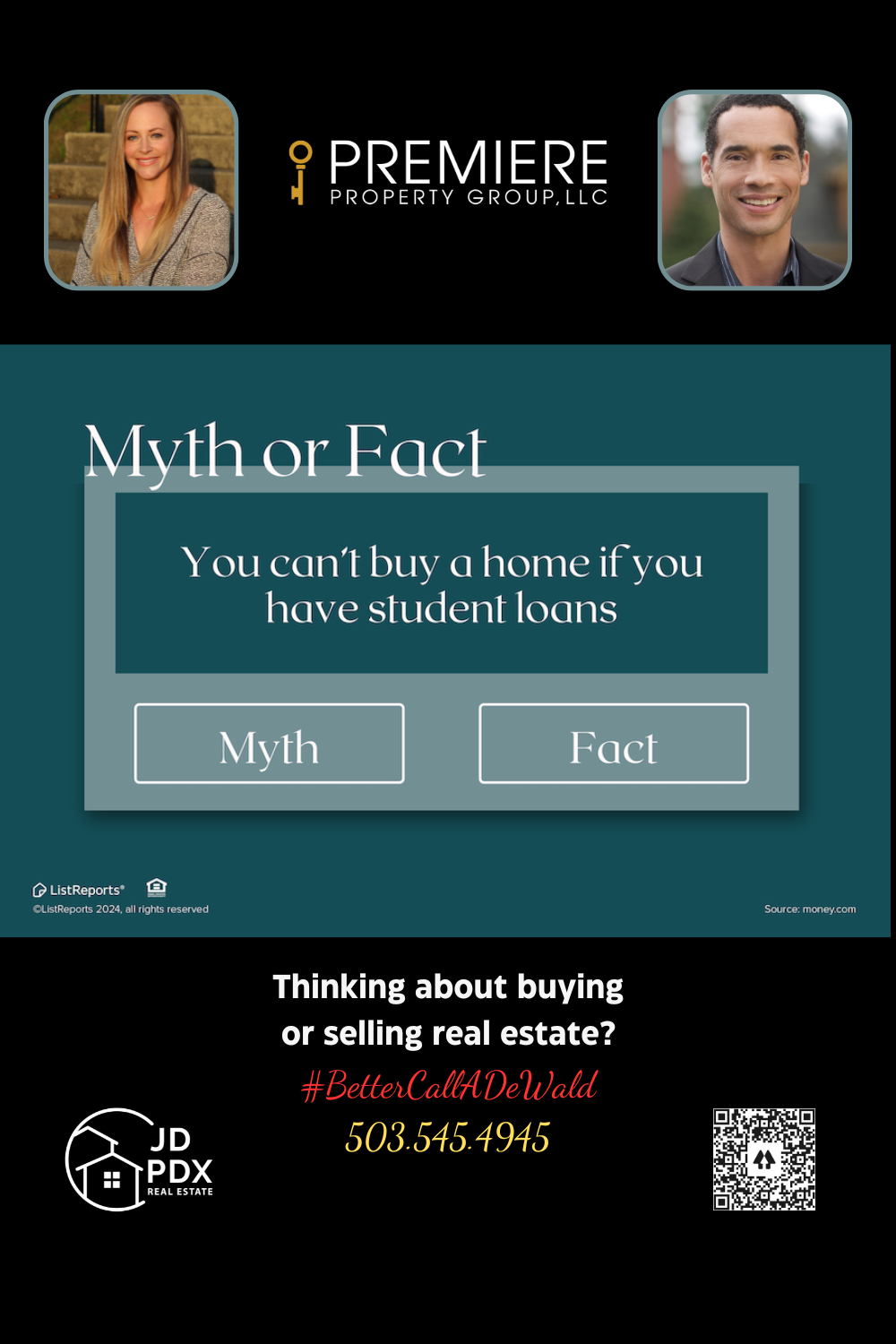

Even if you have student loans, don’t assume that you can’t buy a home. The deciding factor is whether or not you have enough income to cover your student loans, mortgage payments and other debts. Basically, it comes down to your DTI, we can help you sort it – just send us a message!

#BetterCallJamohl 503.545.4945

It Comes Down to Your DTI

If you’re dreaming of buying a home but worried about student loan debt, here’s some good news: having student loans doesn’t automatically mean homeownership is out of reach. The key factor that lenders consider is your Debt-to-Income ratio (DTI)—not just the size of your loans.

Your DTI is the percentage of your monthly income that goes toward paying off debts, including student loans, credit cards, car payments, and your future mortgage. Lenders use this ratio to determine if you have enough income to comfortably manage all your financial obligations. Simply put, it’s about balance.

So, how do you figure out where you stand? Start by calculating your monthly debts and dividing that total by your gross monthly income. Ideally, most lenders prefer a DTI of 43% or lower, though exceptions exist depending on loan programs. Don’t let this overwhelm you—this is where we step in.

We’re here to help you navigate your financial options and determine the best path forward. Whether it’s exploring loan programs designed for buyers with student debt, improving your DTI, or answering your questions, we’ve got your back.

The bottom line? Even with student loans, buying a home is possible. It’s all about understanding your financial picture and taking the right steps to prepare. Let’s connect, crunch the numbers, and make your homeownership dreams a reality.

Ready to get started? Let’s talk about your DTI and create a plan that works for you!

#HomeOwnershipGoals #DTIMatters #BetterCallADeWald

#Homebuyer #JDPDXRealEstate #homeowner #realestate #realestateagent #realtor

Join The Discussion